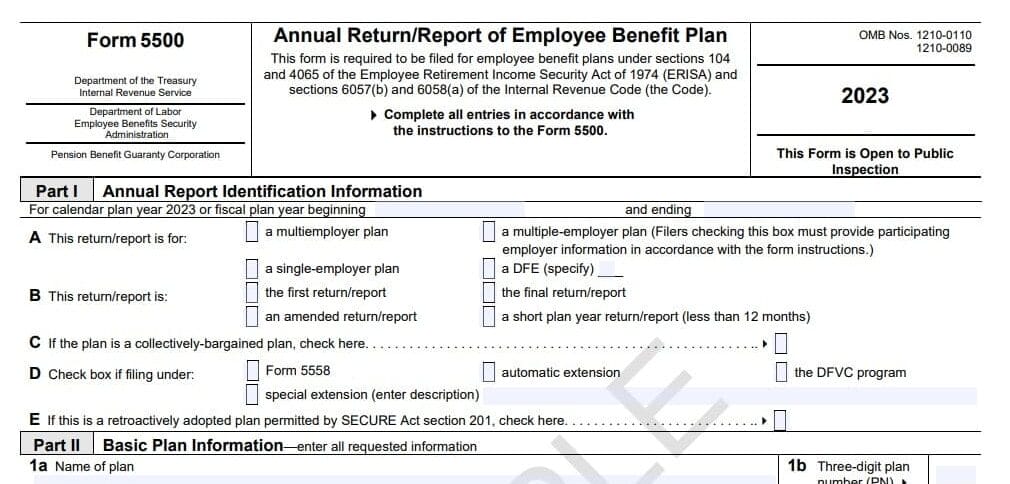

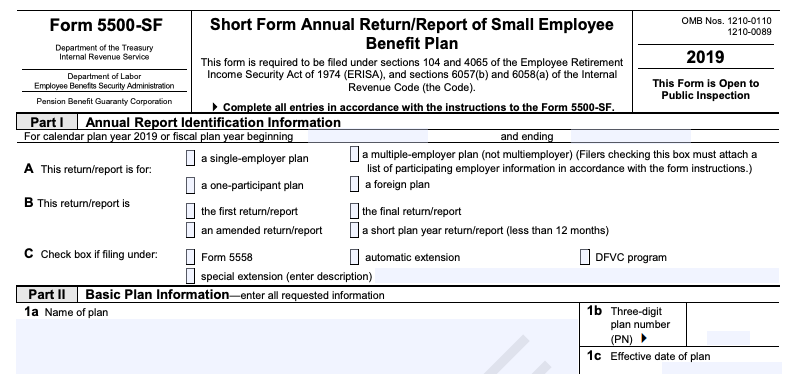

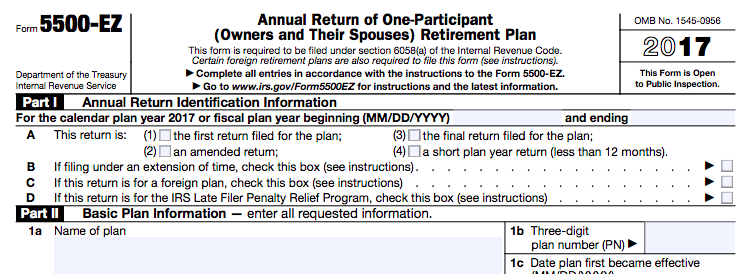

Some employer obligations are apparent, such as providing mandated benefits and following anti-discrimination practices. However, when it comes to compliance documents, things can get confusing quickly (and, not to mention, costly if you miss those deadlines).

One such compliance rule is filing Form 5500. Below is a quick run-down of the ins and outs of the form – including Form 5500 filing requirements, due dates, and versions – to help you remain compliant this year.